Visa Working Capital Index: Asia-Pacific CFOs call for flexible digital finance solutions

|

Amid rising inflation, interest rates, and liquidity pressures, Asia-Pacific Growth Corporates (mid-sized firms with annual revenues between $50 million and $1 billion) increasingly view efficient cash flow management as essential, with working capital becoming a more strategic tool for driving growth and resilience. Yet, nearly half of the region's Growth Corporates are not utilising any working capital solutions, even as companies need more flexible access to cash.

Visa has identified three key themes from the WCI report that are relevant to businesses in Asia-Pacific.

Misalignment between financial products and operational needs

Mid-sized businesses across Asia-Pacific face shifting working capital realities, including longer cash cycles, more structural payment delays and growing pressure to free up cross-border liquidity faster. However, most financial solutions have not kept up, with many remaining too rigid or generic for Asia-Pacific's diverse industries and fast-moving markets.

This growing disconnect between traditional financial product design and the real-world needs of businesses is driving CFOs to call for faster, more flexible and fully digital tools that align with real cash cycles and deliver capital at the speed of business.

Notably, 47 per cent of Growth Corporates do not utilise working capital tools, often because existing solutions do not align with their operational models. At the same time, 41 per cent of firms want simplified digital tools for credit and account management, while 38 per cent seek on-demand financing aligned with cash flow cycles, signalling demand for more flexible financial solutions.

Financial institutions that create offerings around real business cycles, while rethinking underwriting, approval speed and flexibility, will be better positioned to support the evolving needs of Growth Corporates.

Working capital as a strategic growth lever

While many firms lack suitable tools, leading finance teams in Asia-Pacific are treating working capital as a strategic lever rather than a last resort, using early supplier payments, virtual cards and flexible funding to strengthen liquidity and respond more quickly to market opportunities. As a result, cards are evolving from transactional tools into working capital levers.

Accordingly, late customer payments can cost companies an average of $15.7 million annually, but those using card payments to speed up collections have reduced late-payment losses by around 10 per cent. Firms using working capital solutions can realise an average of $17.7 million in annual bottom-line benefits, equivalent to a 4.3 per cent revenue boost. 9 per cent of firms used working capital solutions to fund unplanned growth, up from 5.6 per cent in 2024-25.

By improving cash flow visibility and accelerating receivables, these finance leaders can unlock additional capital within their operating cycles, turning liquidity management into a competitive advantage with direct improvements to the bottom line.

Shifting demands on banks

Across regions, CFOs rank fast, on-demand access to capital and simplified digital credit management among their top priorities, but these needs are especially pronounced in Asia-Pacific, where companies operate in fast-moving and often volatile markets.

61 per cent of Asia-Pacific Growth Corporates now use AI or machine learning for working capital optimisation, including forecasting, risk scoring and automated approvals, as demand grows for embedded analytics and simpler digital credit management within banking platforms.

CFOs expect fast, on-demand access to liquidity through digital rails, including tools such as virtual cards, automated approvals and digital platforms that enable businesses to respond quickly to time-sensitive opportunities. Finance leaders prioritise industry-specific expertise from banking partners, seeking relationship managers who understand sector-specific business cycles, supplier relationships and capital expenditure needs.

These trends signal a shift in how CFOs expect to access and manage liquidity. As demand grows for faster, more flexible financing and digitally enabled finance management, banks and financial institutions will need to move beyond generic products by integrating AI-driven insights, streamlining approval processes and pairing digital capabilities with deeper industry expertise to better support the evolving expectations of Asia-Pacific CFOs.

"CFOs across Asia-Pacific want flexible, sector-specific tools that match their operational realities," said Chavi Jafa, head of Commercial and Money Movement Solutions, Asia-Pacific, Visa.

"Our data shows that agile, digital-first strategies and smarter forecasting are helping companies stay resilient and reinvest freed-up capital into growth. The Working Capital Index continues to spotlight how Growth Corporates are turning volatility into opportunity. At Visa, we are partnering across the ecosystem to deliver tailored, digital-first commercial solutions, like virtual cards integrated in ERP and digital enabler platforms, that help unlock working capital, accelerate approvals, and turn liquidity into a strategic growth lever."

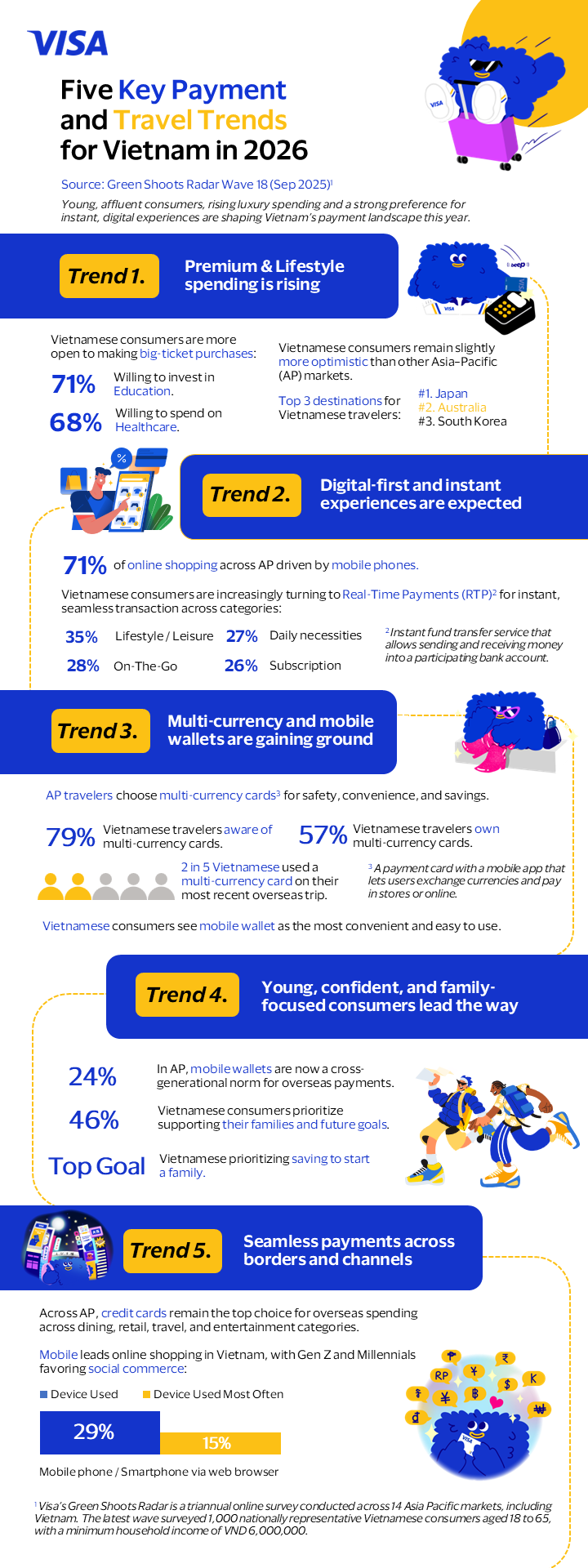

| Visa data highlights five key payment and travel trends in Vietnam for 2026 Visa, a global leader in digital payments, on January 13 released its outlook on the top five trends that will shape how Vietnamese people pay and travel in 2026. |

| Visa and Trip launch global virtual travel card programme Visa and Trip.com entered into a new global agreement designed to make booking and paying for travel more seamless for consumers and partners worldwide on March 17. |

| Visa launches contactless payment system across Hanoi metro network A fully interoperable open-loop payment system has been launched across Hanoi's metro network, enabling Visa cardholders to tap and go on all metro lines in Vietnam. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:

Related Contents

Latest News

More News

- Launch of Vietnam's Vietnam's first non-physical international debit card (June 26, 2026 | 16:14)

- Visa backs Digital Finance Day 2026 to promote safe digital payments (June 08, 2026 | 09:00)

- HSBC and EFA support Nutifood with VND800bn bridge (May 20, 2026 | 10:06)

- Citi entering next phase of AI integration (May 13, 2026 | 18:00)

- Vietnam and South Korea roll out cross-border QR payment service (April 24, 2026 | 10:12)

- CAEX partners with HashKey to build an international-standard digital asset exchange in Vietnam (April 22, 2026 | 19:21)

- VIB approves dividend of nearly 19 per cent (April 09, 2026 | 12:48)

- VIB launches subscription-based Max Card (April 06, 2026 | 10:44)

- HSBC arranges $200m syndicated loan for GELEX Infrastructure (March 30, 2026 | 13:41)

- Visa launches contactless payment system across Hanoi metro network (March 24, 2026 | 10:54)

Mobile Version

Mobile Version