Vietnam to post strong recovery amid external headwinds

Vietnam’s macroeconomic policies should balance supporting recovery while containing inflationary pressures and providing targeted assistance to vulnerable sections of society, according to the 2022 Annual Consultation Report on Vietnam published by the ASEAN+3 Macroeconomic Research Office (AMRO) today.

|

After a sharp slowdown in 2020 and 2021, the Vietnamese economy is expected to rebound robustly in 2022. Manufacturing output continued to expand strongly in 2021, driven by a robust export sector, notwithstanding supply chain disruptions. The increasingly diversified export mix led to the sector’s robust recovery and an increase in the current account surplus. Service income also improved after the border reopened.

In addition, continued strong FDI inflows supported the balance of payments, contributing to a further accumulation of foreign reserves in 2021. Services sector activity has resumed gradually after the easing of mobility restrictions and border controls, but pockets of weakness and an uneven recovery remain.

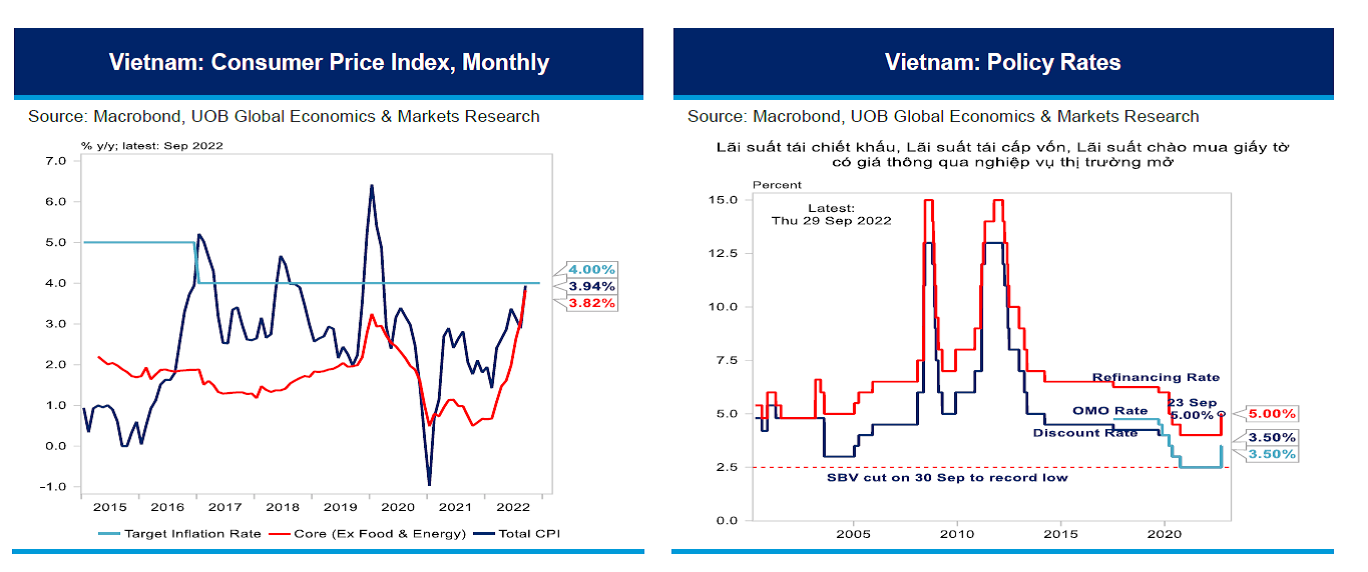

All told, GDP growth is projected at 7 per cent in 2022 and is expected to rise further to 6.5 per cent in 2023. Headline and core inflation have remained low, reflecting price subsidies to contain high global oil prices. Meanwhile, the large GDP revaluation calls for a reassessment of the policy space.

The Vietnamese authorities have employed fiscal policy judiciously since the onset of the pandemic to support growth. The budget shifted to deficits in 2020 and 2021, from near balance in the pre-pandemic period. In January 2022, the National Assembly approved an economic stimulus package to promote economic recovery and raise growth potential. As a result, the 2022 budget, with the stimulus package to be implemented over 2022 and 2023, is set to deliver a strongly expansionary fiscal impulse.

The State Bank of Vietnam (SBV) has maintained an accommodative policy stance in 2021 and 2022. Credit growth has been brisk, against the bank's targeted growth rate of 14 per cent. The exchange rate has been broadly stable against the USD. In the financial sector, regulatory forbearance ended in late June, but interest rate subsidies are provided to borrowers adversely affected by the pandemic under the stimulus package.

Key external risks stem from global supply chain disruptions, flare-ups in more vaccine-resistant COVID variants, tightening financial conditions in advanced economies, and elevated global oil and food prices related to geopolitical developments. China’s zero-COVID approach is likely to continue to strain exports of agricultural products, in addition to creating supply bottlenecks for a range of intermediate goods imports.

Risks in the financial sector may arise from the impact of the pandemic on asset quality. The relatively low NPL ratio partially reflects the SBV’s forbearance policy which expired at the end of June and could unmask weaker underlying credit quality. Separately, potential risks from the real estate sector development warrant close monitoring in the near-to-medium term.

From a longer-term perspective, the pandemic may have widened inequalities across high- and low-income earners, between exported-oriented and domestically-oriented firms, and between large corporations and SMEs. In addition, lasting scars from the pandemic may undermine growth potential over the medium to long term.

| Vietnam is expected to post a strong rebound despite key external risks stemming from global supply chain disruptions, flare-ups in more vaccine-resistant COVID variants, tightening global financial conditions, and elevated global oil prices. |

Given the availability of fiscal space and the uneven recovery across economic and social sectors, fiscal policy should continue to support economic recovery but should target those that continue to be dislocated by the pandemic.

Support measures such as VAT cuts and tax and rental payment delays should be allowed to terminate once the recovery is solid. Infrastructure development will play a critical role in revitalising the economy going forward. Meanwhile, revenue mobilisation should be enhanced to support funding for infrastructure development.

The SBV should normalise monetary policy in tandem with the economic recovery, especially in light of the rising inflationary pressures. This normalisation will also help to contain the build-up of financial imbalances that emerged in an environment of low-interest rates.

Reduction in lending to high-risk segments, especially in the real estate sector, will also be prudent alongside greater efforts to improve the macroprudential and debt resolution frameworks. Efforts are also needed to increase provisioning and capital beyond current guidance to prepare for a potential increase in impaired assets.

Structural reforms should be accelerated to bolster economic recovery and to ensure a sustainable and inclusive development path. As Vietnam progresses beyond the lower middle-income country status, the grant element of concessional financing will decline along with an increasing need to rely on international capital markets to finance development spending.

This will require a concerted effort to implement a broad range of structural reforms to enhance Vietnam’s sovereign rating. Separately, further efforts to develop domestic supporting industries in the manufacturing value chains are needed. AMRO commends the authorities’ commitments to address climate change, and promote financial digitalisation.

| Upgrading Vietnam's GDP forecast for 2022 to 8.2 per cent Against fluctuations in the global political and economic situation that may affect monetary policies and foreign trade in Vietnam, UOB still raised the full-year GDP growth forecast for Vietnam to 8.2 per cent. |

| Strong economic fundamentals are key to fast recovery in Vietnam Vietnam’s economic recovery has been faster than expected and continues despite the challenges of the world's socioeconomic issues. |

| Vietnam's economic growth forecast at 7.5 pc in 2022: World Bank Vietnam’s GDP growth is forecast to expand 7.5 percent in 2022 and 6.7 percent in 2023, with resilient manufacturing and a robust rebound in services serving as the driving forces for economic recovery. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- Polish businesses seek food export opportunities in Vietnam (August 07, 2026 | 08:00)

- Investment boom expected for EU-compliant plastic recycling plants (August 06, 2026 | 08:00)

- MoF outlines strategy to attract high-quality foreign resources (August 04, 2026 | 17:31)

- Six years of EVFTA reshape Vietnam-EU trade ties (August 04, 2026 | 17:06)

- MoF minister outlines priorities for international integration to support growth (August 03, 2026 | 23:24)

- Vietnam’s seven-month trade reaches $659.58 billion as deficit widens (August 03, 2026 | 23:07)

- Vietnam’s reforms earn international recognition as government reviews July performance (August 03, 2026 | 22:52)

- New programme addresses changing startup landscape (August 03, 2026 | 22:45)

- Dutch businesses upbeat about Vietnam's reforms and IFC ambitions (August 03, 2026 | 22:16)

- Vietnam invites Swiss investors to join international financial centre (July 31, 2026 | 14:57)

Mobile Version

Mobile Version