SBV adjustments calm liquidity of currency

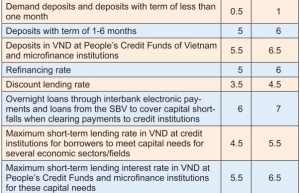

VND deposit interest rates continue to record a strong upward trend of about 0.5-2.8 per cent for most terms across all banks. After the State Bank of Vietnam’s (SBV) decision to increase the operating interest rate by 1 per cent on October 25, all commercial banks in the market have increased their deposit interest rates from 0.5 to 1.8 per cent, focusing on short-term accounts under six months.

In October, around half the banks in the market adjusted their interest rates twice. Some banks, like Techcombank, even raised interest rates three times. Compared to the beginning of the year, the interest rate level on the retail market has increased by 1.5 to 3 per cent. Currently, the deposit interest rate listed is around 7.6-8.2 per cent per year, in which the mobilising interest rate level at state-owned commercial banks is still lower than that of joint stock commercial banks by 0.5-1.7 per cent, per year.

|

| SBV adjustments calm liquidity of currency, source: shutterstock |

In the interbank lending market, at the beginning of October, the overnight lending rate jumped to over 8 per cent, the highest since 2012. However, in the middle of the month, interbank interest rates temporarily cooled when the SBV stepped in to provide market liquidity through open market operations. From November, overnight lending rates were 1.68 percentage points higher than at the end of September.

From the beginning of October to the beginning of November, the SBV net injected more than VND95 trillion ($4.1 billion) through the open market. In particular, there were consecutive sessions where the SBV injected money with longer terms of 14 days.

“Although the volume of transactions in the remaining terms is not significant, there is still a certain amount of liquidity stress for terms of 1-6 months,” said the capital manager of one joint stock commercial bank.

“The SBV has adjusted the monetary policy flexibly and promptly to ensure the objectives of exchange rate stability, inflation control, and the overall safety of the system,” explained a senior leader at BIDV.

“While in the first half of the month, the SBV increased capital injection through open market operation channels and refinancing to support market liquidity after the impact of the SCB event, in the second half of the month, it switched to the channels of treasury bills, selling foreign currencies, and increasing the operating interest rates by 1 per cent to support the exchange rate stability.”

Secondly, he said, the balance of capital credit continued to narrow in October, as capital mobilisation growth continued to face unfavourable foreign currency supply and demand as well as stagnant cash flow in the deposit channel of the State Treasury. According to the SBV, as of the end of October, credit growth reached 11.5 per cent, nearly three times the deposit growth rate of 4.6 per cent.

According to SBV Governor Nguyen Thi Hong, the liquidity of credit institutions is still good, and there is a surplus. In October, the market was mainly affected by psychological factors and complicated movements in the global market.

“Recently, the SBV held several meetings with commercial banks to jointly assess, analyse and identify bottlenecks in the market to have appropriate solutions. Through assessment and analysis, credit institutions also agree that it is necessary to strengthen solidarity, trust, and support to ensure the safety of each bank and the whole system,” Hong said.

She added that all commercial banks in the system had met the operational safety criteria following SBV regulations to respond to recent market concerns.

“The SBV is ready to support in terms of liquidity and ensure the solvency of credit institutions, especially at the end-of-year time. Notably, fiscal tools will be promoted to ease monetary and credit pressures from the banking system,” she said.

Immediately after the interbank interest rate showed signs of cooling, reducing the attractiveness of holding VND, along with pressure on the exchange rate, VND devaluation increased rapidly in October. It is forecast that the trend of central banks increasing rates has not ended, and experts believe interbank interest rates have room to increase.

“Due to the increase in the last months of the year according to the general trend when liquidity demand increases to serve year-end payment needs, there is a possibility that the interbank interest rate will increase again, maybe reaching more than 10 per cent,” said a Vietcombank Securities analyst.

The senior leader of BIDV said that in November, the VND interest rates were expected to continue under increasing pressure, increasing by 0.3-0.5 per cent per year.

“As the international and domestic environment still has many potential risks, especially with inflation and exchange rate pressure, the SBV’s monetary policy will continue to maintain a tightening trend from now to the end of the year, with the priority objective of stabilising the exchange rate and controlling inflation,” he said.

The liquidity story of the VND, although considered to have eased recently, is expected to continue to face difficulties as basic cash flows have not improved. The balance of supply and demand for foreign currency is expected to remain unfavourable, and cash flow will continue to be attracted to the SBV through the channel of bills and foreign currency sales.

At the same time, the credit-capital mobilisation balance is expected to continue to be under pressure, with credit growth expected to accelerate at the year-end, while capital mobilisation growth is still relatively difficult.

Economists believe the room for further increases in interest rates will depend on developments from external factors such as US Federal Reserve movements and developments in the US Dollar Index and Chinese currency. At the same time, internal problems include domestic inflation and devaluation pressure on the VND.

“These factors all support the possibility that the SBV will increase the operating interest rate by at least 50-100 basis points in the fourth quarter of 2022 and the first quarter of 2023. It should be noted that the deposit interest rate is now 1.7-1.9 percentage points higher than the beginning of the year and 20-50 basis points higher than the beginning of 2019,” said economist Le Xuan Nghia.

| State Bank of Vietnam alleviates market pressures The State Bank of Vietnam adjusted several operating interest rates last week, with the move deemed necessary in the context of a strong USD and increasing domestic pressure on interest rates and exchange rates. |

| SBV moves in line with global money-tightening tendency To stabilise the currency rate in the face of fluctuations in the international market, the State Bank of Vietnam (SBV) early last week raised the operating interest rate for the second time in a month. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- Citi Vietnam named Best International Bank by Euromoney (July 22, 2026 | 14:37)

- Logistics firms see diverging Q2 earnings (July 21, 2026 | 18:00)

- Oil and gas firms post strong earnings on project momentum (July 21, 2026 | 17:06)

- Strong Q2 earnings expected to boost investor confidence (July 20, 2026 | 17:24)

- Vietnam's IPO market rebounds with four new listings raising $830million (July 20, 2026 | 08:17)

- BVBank makes HSX debut as Vietnam's banking sector eyes growth (July 20, 2026 | 08:14)

- Capital market reform demands deeper structural changes (July 16, 2026 | 17:39)

- Promising sectors identified for Vietnam's next growth phase (July 16, 2026 | 16:51)

- Reshaping capital flows to unlock Vietnam's next growth engine (July 16, 2026 | 16:35)

- Dragon Capital: Vietnam has 3–5 years to cut bank reliance (July 16, 2026 | 11:58)

Latest News

Mobile Version

Mobile Version