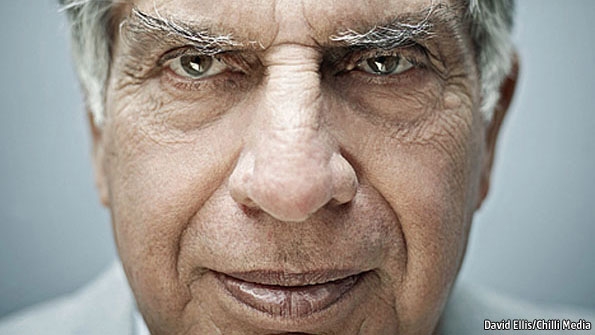

India should learn from the career of its most powerful businessman

The conglomerate he runs is India’s largest private-sector concern, accounting for 7% of the stockmarket. It pays 3% of all India’s corporate tax and 5% of all its excise duty. You can live in a house, drive a car, make a phone call, season your food, insure yourself, wear a watch, walk in shoes, cool yourself with air-conditioning and stay in a hotel, all courtesy of Tata firms. Polite, elegant and reserved, Mr Tata has been the king of India’s corporate scene for the past two decades. Indians look up to him in much the same way that Italians once looked up to Gianni Agnelli at Fiat or Americans did to J.P. Morgan.

In some ways, though, the reverence for Mr Tata is odd. He is not a geekish entrepreneur, like the high-tech wizards in Bangalore. He is an old-style dynast—the fifth generation to run his 144-year-old firm. He took time to grow into the job: when he took the reins in 1991 he struggled to assert himself. Even today, critics accuse him of being regal and secretive—and snipe that the group’s most successful business, TCS, its technology arm, is the one he left most alone.

Nor can Tata be hailed as a financial paragon. After a wave of takeovers during the past decade, its return on capital is mediocre. The new boss, Cyrus Mistry, who comes from outside the family (Mr Tata has no children), may have to reorganise something of a ragbag conglomerate: alongside the stars like TCS or Jaguar Land Rover, a luxury carmaker, there is also a long trail of flabby and indebted businesses (see article).

And yet, for all that, Mr Tata’s career carries two powerful lessons for an introverted and corruption-obsessed India. First, that India has far more to gain than lose from the outside world. And second, that a company can be a force for progress.

The hereditary ruler as hero

Globalisation came easily to Mr Tata, who trained as an architect in America. Even today he would rather discuss car designs with young engineers than read management reviews. That education, and a streak of perfectionism, have served him well. He realised early on that as India’s economy opened in the 1990s its firms would have to raise their standards, benchmark themselves against the very best, and if necessary buy competitors. His foreign takeovers included Corus, a giant British steel firm, and Jaguar Land Rover. The first has been a financial disaster, the second a triumph. But both showed that Indian firms—and those from other emerging economies—deserve their place at the top table of global business.

Indians would love to claim that this lesson has been thoroughly learnt. Names like Mittal and Infosys are known all round the world. But India remains a country with too many protected industries, from shopping to coal mining and newspapers. Mr Tata himself was not always as keen to open up at home as he was to venture abroad. But for the most part he was a firm advocate of globalisation.

The other lesson from Mr Tata has to do with integrity. His group has not entirely avoided scandals. It faced a rogue trader in the early 2000s, and did not completely escape the furore over the bent award of telecoms licences in 2008. No doubt somewhere today, in this firm with $100 billion of sales, funny business is taking place. Rivals grumble that Tata’s current respectability masks a past spent toadying up to politicians in the years before and after India’s independence in 1947. But the fact is that Mr Tata, in public, and by widespread repute in private too, has stood against corruption. His attitude towards India’s political class has been one of polite distance. He has long attacked what he calls “vested interests”—code for crony capitalism, in which firms make profits by buying favours from officials and politicians.

Looking in the mirror

Crony capitalism has seldom seemed more of a threat to India. Back in the 1990s, the country’s leading firms—technology companies as well as Tata Sons—went to extraordinary lengths to be squeaky-clean. Family firms, which still control about 40% of India’s stockmarket profits, professionalised their management and listed their shares. But over the past decade things have gone backwards. The new money has been made in “rent-seeking” sectors, such as mining and infrastructure, with a lot of government involvement and little foreign competition; some mouth-wateringly large corruption scandals have occurred there. Too many family firms have lost interest in improving governance. Some, unwilling to relinquish control by issuing shares, have piled on debt, and now that they are in trouble, are bullying state-run banks to “extend and pretend”—roll over their loans rather than write them down. Such firms thus become state-supported zombies.

The Indian public is fed up. Anti-corruption agencies are newly vigilant. Business has become a hall of mirrors in which fingers point everywhere. Suspicion is so pervasive that even clean officials are terrified to prod along vital projects by clean companies for fear of being accused of favouritism.

The problems in parts of the private sector have thus become a macroeconomic issue. Investment by private companies has slumped—the main reason why economic growth has slowed from 10% to about 5.5%.

It is easy to blame all this on corrupt politicians. But somebody is paying the bribes. By standing out against graft so publicly and consistently, Mr Tata was ahead of his time. The irony is that by doing so he was preparing the way for the end of businesses such as his own. As India’s economy modernises and becomes more open and transparent, the rationale may disappear for sprawling, hereditary conglomerates, which use the bonds of kin to deal with a shortage of trust, and pool their managers and capital because the outside markets for these resources do not work well.

To that extent, Mr Tata may come to be seen as both the last of one breed of feudal corporate leaders—and the first of another more open bunch. Anybody who cares about India’s future, especially its billion consumers, should hope that the transition picks up speed again.

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- The generics industry: unlocking new growth drivers (February 04, 2026 | 17:39)

- Vietnam ready to increase purchases of US goods (February 04, 2026 | 15:55)

- Steel industry faces challenges in 2026 (February 03, 2026 | 17:20)

- State corporations poised to drive 2026 growth (February 03, 2026 | 13:58)

- Why high-tech talent will define Vietnam’s growth (February 02, 2026 | 10:47)

- FMCG resilience amid varying storms (February 02, 2026 | 10:00)

- Customs reforms strengthen business confidence, support trade growth (February 01, 2026 | 08:20)

- Vietnam and US to launch sixth trade negotiation round (January 30, 2026 | 15:19)

- Digital publishing emerges as key growth driver in Vietnam (January 30, 2026 | 10:59)

- EVN signs key contract for Tri An hydropower expansion (January 30, 2026 | 10:57)

Mobile Version

Mobile Version