Credit growth rate might pose risks

|

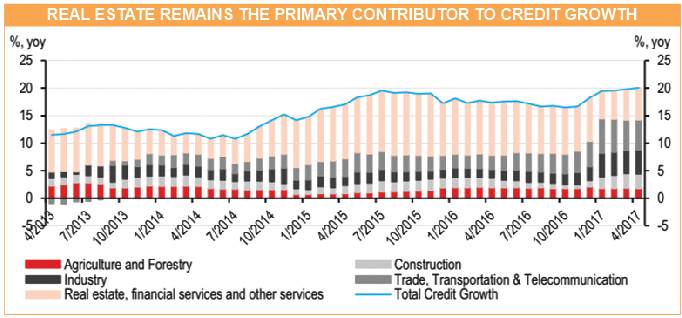

| Source: CEIIC, IMF and HSBC |

The favour of loans

Noelan Arbis, an economist for the ASEAN region at HSBC, said in his latest report on Vietnam’s economics that “Vietnam could easily reach a 21 per cent credit growth rate by the end of the year.”

But the report followed by saying that the higher rate “may pose considerable risks” to the economy, given the lingering issues of legacy non-performing loans (NPLs) and the quality of credit that could be created in reaching the new target.

Arbis’ confidence in Vietnam being able to accomplish said credit growth target is based on the current pace of credit growth, which reached 11.5 per cent at the end of August according to the National Financial Supervisory Commission, and the central bank’s rate cuts in July.

As for risks, he pointed to the fact that the allocation of credit has leaned toward less productive industries such as real estate, and toward state-owned enterprises (SOEs), at the expense of small- and medium-sized enterprises (SMEs).

“The allocation of credit is important, as Vietnamese SMEs compete for funding with SOEs and large private corporations,” he said.

Hanoi-based vice president and CEO of Phu Quy Agricultural Farm JSC Nguyen Thi Le Na voiced similar concerns during a seminar on agriculture lending held in July. Na manages a citrus orchard, an SME worth several billion VND in Nghe An province. She told VIR that it has never been easy for a small firm like hers to get access to loans at favourable interest rates.

To Hoai Nam, secretary general of the Vietnam Association of Small- and Medium-sized Enterprises, noted that about 70 per cent of SMEs are not sufficiently financed.

SMEs vs SOEs

The HSBC economist, citing recent studies conducted by the World Bank and International Monetary Fund (IMF), pointed to the fact that SOEs are absorbing a disproportionate amount of credit in the Vietnamese economy at the expense of SMEs.

“In Hanoi, for instance, the majority of loans still go to state-owned firms. An empirical study from the IMF also shows that SOEs borrow at lower interest rates than private firms, enabling weak SOEs to access bank funding to avoid shrinking their balance sheets,” the report read.

“Meanwhile,” it continued, “a World Bank survey of Vietnamese enterprises showed that only 29 per cent of small enterprises (1-20 employees) have an active credit line, with SOEs and large domestic companies taking the lion’s share of credit in the market.”

Such data, in Arbis’ opinion, suggests that high credit growth alone is not enough to lift Vietnam’s economic growth. The misallocation of credit and the crowding out of private investment may weigh on GDP growth and increase the risk of future NPLs if left unchecked.

In addition, the decline of the NPL-to-total loan ratio in recent years somewhat belies the true level of problematic loans in the economy. Part of the reduction in NPLs is due to transfers to the Vietnam Asset Management Company, where the underlying risk of such loans still lurks.

According to Arbis, rapid credit growth may create new risks for the banking sector, especially if new credit is placed in less productive industries such as real estate-related sectors. These sectors still appear to be contributing the most to total credit growth, despite their declining contribution in recent months.

“The country’s real estate sector, which sank after a bubble period in 2006-2008, was one of the primary reasons for a rise in NPLs and the country’s banking sector crisis in 2011,” he added.

Rocky road

Although a boom in credit means that the Vietnamese economy is recovering well, experts are concerned that the revised growth target of 21-22 per cent may do more harm than good. At a conference held in early September in Ho Chi Minh City, head of the Vietnam Institute of Economics Tran Dinh Thien emphasised that credit expansion does not always go hand-in-hand with GDP growth.

“A credit boom usually causes an immediate hike in inflation rates before it can help boost GDP. In my opinion, the bubble period that just ended a few years ago may return if we’re too occupied with pumping money into the economy,” Thien told VIR. In 2010, credit in Vietnam grew by 30 per cent a year and inflation soared to 12 per cent. The bubble soon burst afterwards, leaving banks with a pile of bad debt that remains to this day.

Thien believes that besides commercial lending, Vietnam can make use of more sustainable tools to drive the economy forward. Selling SOEs to private investors, improving business conditions, and attracting foreign investments are some of the options, according to the economist.

Pham Hong Hai, CEO of HSBC Vietnam, shared the same concerns about the implications of expanding credit. Reports from the bank showed that after a calm period, there will be upside risks to inflation in the latter half of 2017 as healthcare and education costs continue to rise.

“As Vietnam pushes credit growth, the country should maintain a close watch over its consumer price index, which is on the upward trajectory. I think that Vietnam is in greater need of a comprehensive reform of its business environment rather than another risky credit boom,” Hai said.

It is notable that despite a rise in credit and heightened competition among different lenders, lending rates in Vietnam remain some of the highest in Asia. Nguyen Thi Mai Thanh, chairwoman of state-owned REE Corporation, expressed her hope that Vietnam would focus on lowering interest rates to assist domestic firms.

“Lending rates in Vietnam stand at 10 or 11 per cent, while banks in other countries in the region only charge 4 to 5 per cent. This means Vietnamese businesses are at a disadvantage compared to overseas rivals, and we sincerely hope that this matter will take priority along with credit growth,” Thanh said.

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Latest News

More News

- Citi: Vietnam’s economy remains resilient in 2026 (August 03, 2026 | 11:06)

- FX pressures to persist but remain manageable in H2: HSBC (August 02, 2026 | 08:00)

- Citi Vietnam hosts AI Day to equip staff with digital skills (July 31, 2026 | 11:04)

- Fed holds rates steady for fifth straight meeting (July 30, 2026 | 17:30)

- Vietnam stocks rebound as analysts retain bullish outlook (July 30, 2026 | 16:39)

- Q2 earnings paint mixed picture across listed firms (July 30, 2026 | 16:37)

- MB chairman: Vietnam can be testing ground for globally scalable innovation (July 30, 2026 | 14:33)

- Manufacturing firms deliver stronger earnings on efficiency gains (July 30, 2026 | 12:40)

- Investment Support Fund Management Council reshuffled (July 30, 2026 | 12:18)

- Vietnam and World Bank align on 2026-2030 high-impact project lending pipeline (July 30, 2026 | 12:06)

Mobile Version

Mobile Version