Life insurance market heats up despite slowing new sales

According to latest Global Insurance Market Bulletin released by the Insurance Supervisory Authority under the Ministry of Finance, total insurance premium revenue across the market in the first two months of 2026 was estimated at $1.41 billion, up 1.13 per cent on-year. Of the total, life insurance premium revenue was estimated at $760.1 million, down 5.27 per cent.

") |

New business premium revenue in the life insurance segment during the two-month period was estimated at more than $109.4 million, marking a 12.5 per cent decline on the same period last year. However, market share movements reflected increasingly fierce competition within the sector.

Bao Viet Life maintained its leading position, although its market share continued to narrow, falling from 21.4 per cent for full-year 2025 to 18.3 per cent in cumulative terms during the first two months of 2026.

Meanwhile, Generali drew attention after accelerating strongly in January with a market share of 17.07 per cent, placing it among the market leaders, before easing to 11.5 per cent after two months.

Dai-ichi Life and AIA continued to show stability among the top-tier insurers, each holding around 11-12 per cent market share.

Meanwhile, Techcom Life emerged as a notable player, entering the industry’s top five in terms of new business premium revenue.

Its market share rose from 7.08 per cent in January to 8.3 per cent in February, surpassing several long-established foreign insurers such as Prudential and Manulife.

MB Life, Prudential, and Manulife, meanwhile, maintained relatively stable market shares of around 6-7 per cent.

In terms of total life insurance premium revenue, Bao Viet Life remained the market leader with a 23.5 per cent share, followed by Manulife at 17.4 per cent, Dai-ichi Life at 11.8 per cent, AIA at 11.6 per cent, and Prudential at 11.4 per cent.

Other insurers such as Generali, FWD, MB Ageas, Hanwha, Cathay, Sun Life, and Techcom Life accounted for smaller shares, yet competition among them has become increasingly aggressive.

Regarding product structure, data from the Insurance Supervisory Authority showed that investment-linked insurance products continued to account for the largest proportion, contributing 60.3 per cent of new business premium revenue during the first two months of the year.

This was followed by term life insurance at 6.11 per cent and endowment insurance at 5.99 per cent. Other product lines such as whole life insurance, pension insurance, and health insurance accounted for only around 0.53 per cent.

In addition, revenue from bundled insurance products contributed as much as 27.07 per cent of total new business premium revenue across the market.

In terms of policy numbers, the market recorded 194,253 new contracts during the period. Term life insurance led with 94,677 contracts, accounting for 48.7 per cent, followed by investment-linked insurance with 81,344 contracts, equivalent to 41.8 per cent.

Endowment insurance reached 10,311 contracts, representing 5.3 per cent, while other product categories accounted for approximately 4.08 per cent.

A senior industry expert said the strong growth in term life insurance was driven by its low premiums, accessibility, and ability to meet pure protection needs rather than investment objectives, particularly after a period of significant market volatility.

As of the end of February 2026, the total number of in-force contracts across the market, excluding bundled insurance products, stood at 11.37 million, down 3.36 per cent on-year.

Within the overall life insurance premium revenue structure, investment-linked insurance continued to dominate with a 72.4 per cent share, followed by endowment insurance at 12.3 per cent, while bundled insurance products contributed around 13.8 per cent of total market premium revenue.

According to Nguyen Anh Tuan, deputy CEO and chief of Retail Banking at Techcombank, 2023-2024 was a difficult phase for Vietnam’s life insurance market following years of rapid growth, as many products and services had not fully matched customers’ needs and income levels.

“The Vietnamese life insurance market still holds enormous potential, as insurance penetration currently stands at only around 7-8 per cent. Alongside the trend of per capita income continuing to rise to $6,000 per person, demand for life insurance products is expected to edge up, similar to many countries with comparable income levels. Life insurance penetration in Vietnam could entirely reach 20-30 per cent within the next few years, helping address the market’s scale limitations,” he said.

| Rising demand for financial protection fuels life insurance growth Vietnam’s life insurance market is entering a new phase of sustainable growth following a comprehensive restructuring of products, distribution channels, and customer services. In an interview with VIR’s Anh Duc, Bae Seung Jun, general director of Shinhan Life Vietnam, shared his positive assessment of the market outlook and outlined the company’s strategy to address customers’ genuine insurance needs. |

| Insurance market splits in Q1 amid market divergence Vietnam’s insurance market showed modest growth in Q1, 2026, but a sharp divide emerged as non-life expanded on rising protection demand while life insurance continued to struggle under inflation-driven shifts in consumer behaviour. |

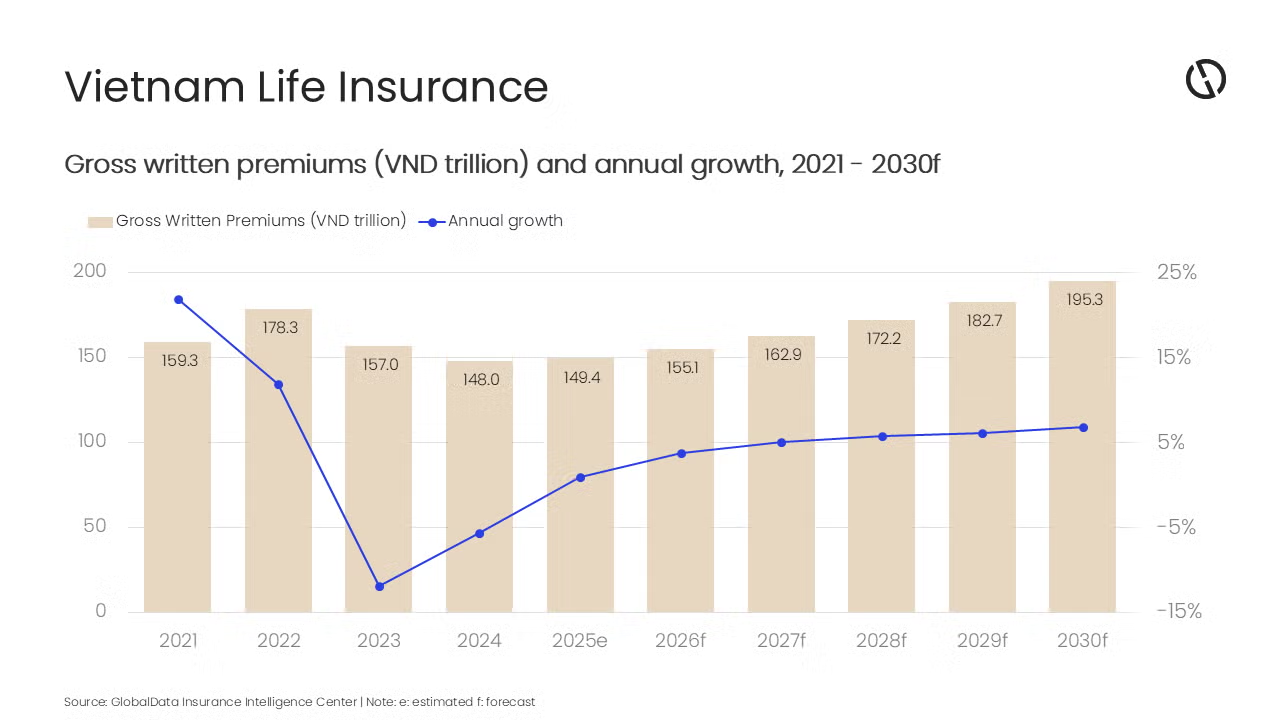

| Vietnam's life insurance industry to surpass $7 billion by 2030 Vietnam's life insurance industry is projected to grow at a compound annual growth rate of 5.9 per cent, increasing from $6 billion in 2026 to $7.2 billion by 2030 in terms of gross written premium, according to a report by GlobalData on April 15. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:

Related Contents

Latest News

More News

- NNX opens first insurance centre in Hanoi (July 08, 2026 | 16:17)

- Vietnam to unlock long-term savings through expanded pension fund (June 11, 2026 | 14:04)

- Infrastructure boom fuels expansion of non-life insurance market (June 06, 2026 | 14:40)

- Igloo expands into life insurance with Chubb Life partnership in Vietnam (June 06, 2026 | 11:25)

- Vietnam targets 25 per cent micro-insurance coverage by 2030 (June 05, 2026 | 14:42)

- Willis and Global Parametrics deliver payouts to coffee farmers hit by storms (May 22, 2026 | 09:39)

- Insurance shareholders push for higher dividends in 2026 (April 24, 2026 | 12:21)

- Vietnam's life insurance industry to surpass $7 billion by 2030 (April 16, 2026 | 14:26)

- Non-life insurance competition heats up as smaller players gain ground (April 16, 2026 | 14:25)

- Insurance market splits in Q1 amid market divergence (April 08, 2026 | 23:46)

Mobile Version

Mobile Version