How the SBV deals with climate risks

Most central banks now consider climate change as too important – and they are acting. In Asia, the People’s Bank of China, the Bank of Japan, the Bank Negara Malaysia, and the Monetary Authority of Singapore have already adopted climate strategies.

|

| Banks are being required to collect more information, especially when it comes to sustainability, Le Toan |

In Vietnam, the central bank has successfully supported economic growth. However, by doing that, the State Bank of Vietnam (SBV) has also contributed – unintentionally – to fast-rising greenhouse gas (GHG) emissions.

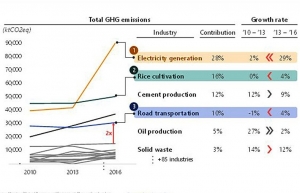

The elasticity of CO2 emissions to growth is as high as 1.5 in Vietnam. In other words, carbon emissions increase by 1.5 per cent when GDP grows by 1 per cent. The country’s economic take-off has been strong, but this has raised its CO2 emissions to a high level of 326 million tonnes in 2021, more than Thailand, Indonesia, and Malaysia. A paradigm change is needed. Economic growth and carbon emissions must be decoupled. For this, the SBV can help.

The central bank law adopted in 2010 contains broad objectives: stability of the currency, soundness of credit institutions, safety and effectiveness of the payments system, and socioeconomic development. Climate change and the energy transition affect all these dimensions.

The SBV would therefore be well within its mandate when adjusting its policies to support the mitigation of, and adaptation to, climate change. What matters is that policymakers keep climate on their mind at all times.

Facing climate risks

Vietnam faces considerable climate-related risks. The World Bank has warned of possible disasters stemming from flooding, tropical cyclones, drought exposure, and heat waves. Vietnamese people are accustomed to harsh weather events, but upcoming hazards will be worse than in the past.

Agriculture will be particularly at risk of saline water intrusion and crop failure. Urban areas will be exposed to periods of extreme heat, which will reduce workers’ productivity or make outdoor labour unhealthy. Residential and commercial properties located near the coastline and close to large riverbanks will be at risk of flooding. Credit institutions are exposed to these adverse developments through their loan portfolios – such as mortgage loans and holding of corporate bonds.

Apart from these physical risks, banks are also exposed to “transition risks” such as carbon-emitting borrowers running into financial difficulties following fast changes in climate policies, technology, and consumer preferences.

A fast-rising demand for renewable energy would create difficulties for firms relying on fossil fuels. The traditional connections between state-owned banks and state-owned energy utilities would aggravate the risk.

Banks need to anticipate these risks. This requires changes in many dimensions: risk assessment, data collection, modelling, strategy, and governance. Banks need to conduct portfolio analysis and determine their exposure to climate risks.

Making sustainable reporting mandatory is key: companies should be required to collect and publish non-financial information, including on their environmental impacts – such as energy efficiency, GHG emissions, biodiversity conservation, water usage, and recycling practices.

To ensure credibility, reporting must follow established guidelines, such as guidance issued by the Taskforce on Climate-Related Financial Disclosures or by the International Sustainability Standards Board. Third-party auditing and certification are also important to establish credibility and avoid greenwashing.

To enforce these good practices, the SBV can use its supervisory power. It has already required banks to create by 2025 departments dedicated to climate analysis, and many banks have followed suit. But it can go further: international supervisory bodies recommend setting supervisory expectations on how banks must manage climate risks.

These expectations define minimum standards that banks must implement to address climate risks adequately throughout all their activities. They cover governance structure, risk management processes, tools, and metrics to use, as well as disclosure requirements.

In addition, the SBV has microprudential and macroprudential tools available to maintain financial stability. In this context, the International Monetary Fund (IMF) has urged Vietnam’s supervisors to assess the capacity of banks to absorb potential losses, with a focus on non-performing loans, provisions, and profitability prospects. Such assessment is also warranted for the exposure of banks to climate-related risks.

Capital requirements are key for the resilience of banks. The SBV must ensure that climate risks, as with any other financial risks, are reflected in capital requirements. The SBV could also rely on macroprudential tools like systemic risk buffers to address climate risk at the level of the banking system.

Decarbonising SBV’s domestic operations

The SBV can do more than analyse climate risks: it can contribute to preventing them with its refinancing operations. The central bank already directs credit to specific sectors such as small- and medium-sized enterprises and agriculture, in accordance with government priorities. It does so with its refinancing instruments, lending to credit institutions at lower interest rates for loans to targeted sectors.

In 2018, the SBV launched the Green Banking Development Scheme, which encourages credit institutions to expand their loan portfolio to green investments, together with guidance on how to improve staff training, corporate strategy, and analytical tools such as data and models. However, guidance remains general, and implementation measures are not yet clearly spelt out. As a result, green bank credit remains only 5 per cent of total credit – too little to make it count.

The SBV could study the practice of People’s Bank of China (PBC) when it comes to proactively using monetary policy to steer funding to targeted segments of the economy. The PBC uses a range of policy instruments to focus on targeted sectors, such as micro- and small-sized businesses and rural firms with limited access to financial markets. The PBC also provides targeted funding to institutions that lend to carbon-reduction technology and clean energy projects, with an interest rate much lower than offered in other lending facilities.

These interventions follow market principles, such as creating financial incentives for banks, while leaving the default risk of these loans with the banks, which encourages due diligence and avoids moral hazard. This is different from traditional administrative interventions that direct credit to specific borrowers, at the risk of encumbering the banking system with non-performing loans and delinquencies.

Outside China, other central banks also use a variety of instruments to encourage lending to decarbonisation projects. As an illustration, the Bank of Japan has a lending facility to commercial banks with a lower interest rate conditional on their green, transition, and sustainability-linked loans and bond investment performance.

The European Central Bank is also putting in place an ambitious programme to decarbonise its corporate bond holdings. It will also reflect climate-related risk in the haircut applied to collateral, and has extended collateral eligibility to some sustainable finance securities.

The SBV could also consider building its own portfolio of green bonds and sustainability-linked bonds. The central bank conducts open market operations with a focus on government securities and its own securities. Hence, it has scope to broaden, diversify and decarbonise its portfolio.

It could do so with purchases of green bonds and sustainability-linked bonds. These green securities can be issued by the central government, municipalities, and state-owned enterprises – hence the SBV does not need to invest in private-sector securities if it does not wish to do so.

Greening foreign exchange reserves

Gross foreign exchange reserves held by the SBV will grow to $125 billion by the end of 2022 according to IMF projections – a large financial buffer that builds confidence in its ability to stabilise the currency.

The management of foreign exchange reserves typically follows three rules: liquidity, safety, and return. Liquidity is important to react quickly to sudden market volatility; safety is essential to protect these hard-won assets; return matters so that the central bank does not operate at a loss.

The second rule, safety, needs to take climate risks into account. For this, the SBV should disinvest from high-carbon assets, which are more exposed to transition risks, and gradually build up a portfolio of foreign-currency-denominated sustainability assets.

This is easier said than done. Expertise is required to select adequate assets, avoid greenwashing, and ensure that the three rules of liquidity, safety and return remain fulfilled.

The Asian Green Bond Fund launched by the Bank of International Settlement in early 2022 could be a first vehicle to gradually green the SBV’s foreign reserves. The fund consists of high-quality bonds issued by sovereign, international, and corporate issuers that comply with strict green standards. By investing in the fund, the SBV would follow the lead of the Bank Indonesia, which is supporting the initiative.

The upcoming threat of climate change must be met with a vigorous response from all. Thus, Vietnam’s central bank should do its part, help to decarbonise economic growth, and protect the banking system from upcoming climate risks.

|

| Pierre Monnin, senior fellow and Patrick Lenain, senior associate of the Council on Economic Policies |

| Acute challenge for world to tackle climate crisis at COP27 The biggest climate summit ever will test the resolve of nations to combat climate change, with many of the biggest influencers distracted by crisis, and developing countries clamouring for assistance. |

| Time is now for leaders to grasp climate breakthrough The outcome of the COP27 climate conference in Egypt hangs in the balance as nations scramble to issue stronger commitments and agree on the next steps to save the planet. |

| Innovating towards net zero: energy, rice, and transportation in Vietnam Vietnam is striving to hit its net zero targets by 2050, and there are certain industries which should be focused on. |

| New balance required in exploitation of fossil fuels With global challenges on climate change as well as international commitments on emission reduction, Vietnam will require a strategy to effectively use coal power and follow suit with its goals. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- Citi: Vietnam’s economy remains resilient in 2026 (August 03, 2026 | 11:06)

- FX pressures to persist but remain manageable in H2: HSBC (August 02, 2026 | 08:00)

- Citi Vietnam hosts AI Day to equip staff with digital skills (July 31, 2026 | 11:04)

- Fed holds rates steady for fifth straight meeting (July 30, 2026 | 17:30)

- Vietnam stocks rebound as analysts retain bullish outlook (July 30, 2026 | 16:39)

- Q2 earnings paint mixed picture across listed firms (July 30, 2026 | 16:37)

- MB chairman: Vietnam can be testing ground for globally scalable innovation (July 30, 2026 | 14:33)

- Manufacturing firms deliver stronger earnings on efficiency gains (July 30, 2026 | 12:40)

- Investment Support Fund Management Council reshuffled (July 30, 2026 | 12:18)

- Vietnam and World Bank align on 2026-2030 high-impact project lending pipeline (July 30, 2026 | 12:06)

Mobile Version

Mobile Version