GenAI can drive success in banking

The assessment comes from a PwC survey on the assessment of GenAI’s impact over the next three years, published at a banking conference on data-driven success on September 19 in Hanoi.

|

| GenAI can drive success in banking |

“Banking systems hold a vast and invaluable amount of customer data, especially sensitive financial and transactional information, which can become highly significant if managed and used correctly. This is particularly crucial as banks increasingly adopt new technologies such as big data, AI, and machine learning,” said Nguyen Thanh Son, director of the Training Centre at the Vietnam Banks Association.

In transforming and adopting a very different way of operating with GenAI, the finance function will become significantly more efficient and have the opportunity to actively contribute to business performance and drive real value creation.

“Today, banks face a landscape of complex systems, legacy applications, and ever-expanding data. Active metadata offers a solution by connecting bank terms with technical metadata, creating meaningful relationships between data elements and bank’s context,” said James Penfold, pre-sales and technical account management of US group Ab Initio Software.

“This connection enables banks to manage data more effectively, such as automatically masking sensitive information like credit scores. By linking business terms such as customer phone number with technical elements, banks can enforce data protection rules automatically, ensuring consistency across systems,” he added.

GenAI use cases have significant benefits within banking functions across transformation, documentation, and analytics, evidenced by a multitude of publicly documented use-cases currently in development by Tier 1 banks, across all GenAI patterns, according to the PwC 2024 Global CEO Survey for Asia-Pacific.

“Active metadata also streamlines data management processes, allowing banks to auto-generate data pipelines, quality rules, and data governance procedures. Instead of manually creating rules and pipelines, these processes are automated based on business logic, saving time and resources. For example, credit score data can be automatically masked or encrypted, depending on where it resides,” said Penfold.

According to a report by Statista in August, the banking industry’s investment in GenAI is projected to reach $85 billion by 2030, growing at an annual rate of over 55 per cent.

From this forecast, Bui Thi Ngoc Thuy, director of Financial Services at PwC Vietnam, noted that there are key areas of GenAI in the banking industry that credit institutions in Vietnam need to focus on implementing and continuously upgrading in the near future, including customer services, product research and development, automated compliance, due diligence support, and risk management.

“Vietnamese banks can utilise GenAI in combination with conversational AI solutions to provide or enhance existing chatbot or virtual assistant interfaces. It can add value to the bank’s processes of identifying, assessing, and mitigating risks to protect against financial losses. It can also be used to screen related transactions to detect potential risk violations and fraudulent customer behaviour,” said Dung.

Effectively managing GenAI in the banking sector helps create personalised financial products and offers in retail banking, private banking, and corporate banking, tailored to the specific needs and preferences of each customer to generate new competitive advantages. Automating processes to evaluate complex data and models to determine whether an applicant’s information is reliable and aligns with the bank’s risk appetite.”

However, banks in Vietnam also need to recognise the importance of understanding AI risks as societal, market, and regulatory forces are introducing unique risks amplified by the scale and speed of GenAI.

“Applying cutting-edge technological solutions within the Vietnamese banking system enables them to fully leverage data platforms and analytics for better governance decisions and improved business operations, but also introduces significant operational risks,” said Le Thanh Hai, vice president of tech solutions company SVTech.

“Integration challenges can create operational inefficiencies, and the complexity of managing AI-related cybersecurity risks can overwhelm banks lacking expertise. Without skilled personnel, vulnerabilities may increase, highlighting the need for investment in training and resources.”

Dinh Hong Hanh, deputy general director and leader of Financial Consulting Services at PwC Vietnam, added, “Legal and privacy risks are equally concerning. Privacy violations may arise from processing personal data without explicit consent, leading to legal consequences. Data breaches and surveillance practices can result in the misuse of personal information, undermining consumer trust.”

| Jirath Hirunpaphaphisoot, director, Financial Service Strategy and Operations PwC Thailand

Strategic use of big data positions banks for sustained long-term success. By harnessing big data, banks are not only boosting revenue but also fostering stronger customer relationships. Through a combination of internal and external data, banks develop comprehensive customer profiles, allowing them to effectively segment their clientele. This enables hyper-personalisation, where products like loans and investment options are tailored in real-time to meet individual needs, significantly enhancing customer satisfaction and promoting cross-selling and upselling opportunities. Big data also transforms marketing efforts. AI-driven algorithms analyse online behaviours and social trends, enabling banks to run targeted campaigns, draw in customers, and optimise marketing expenditures. In terms of customer retention, machine learning models identify potential churn by analysing customer behaviour, allowing banks to proactively intervene with personalised offers. Moreover, by addressing friction points in customer interactions, banks improve the overall customer experience. On the risk management front, big data is pivotal in detecting fraud in real-time and refining credit scoring, using non-traditional data to expand access without increasing risk. With cloud technology and data lakes, banks now have the infrastructure to process vast amounts of data efficiently, ensuring scalability and compliance with ever-evolving regulations. Nguyen Ngoc Bien, deputy head, Virtual Assistant Tech AI Centre, MBBank

Looking ahead, MB Bank is actively researching ways to implement AI solutions in fraud detection within the operations division. By the end of the year, the bank aims to integrate these models to enhance customer protection and drive cross-selling opportunities. This strategic approach reflects MB’s vision of positioning AI at the core of its operational and customer-centric initiatives. MB has integrated AI across various models, including credit limit allocation, credit assessment, and personalised marketing products. Recently, the bank established an AI centre dedicated to supporting its IT division in managing data operations for tens of millions of customers. This move underscores MB’s commitment to leveraging data-driven insights and enhancing operational efficiency. Last year, MB introduced a strategic initiative focused on auto loans. The AI and analytics centre utilised AI tools to identify potential customers, while also developing AI models to predict customer churn, assess customer capacity, and detect those with a growing demand for vehicle purchases. |

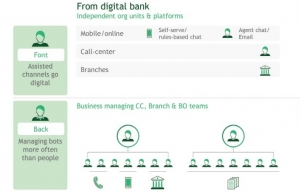

| GenAI’s impact on the financial sector Vietnam’s financial sector has shown remarkable growth, accompanied by a rising demand for digital services. Managing director and partner Il-Dong Kwon and project leader Luan Nguyen of Boston Consulting Group explain that a comprehensive strategy is imperative in order to bolster competitiveness. |

| GenAI’s effect on governance, risk, and compliance The domain of governance, risk, and compliance (GRC) has been experiencing an increase in complexity from multiple angles, and rightly so; but, until recently, the domain wasn’t technologically disrupted. Generative AI (GenAI) has opened a plethora of possibilities for its utilisation in conjunction with GRC, and the industry is racing towards its democratisation. |

| Siemens collaboration unlocks the power of GenAI AI is now being applied on a large scale for industrial development. Dr. Pham Thai Lai, CEO of Siemens ASEAN and Vietnam, spoke with VIR’s Thanh Dat about how to unlock the power of Generative AI, with the participation of Siemens Industrial Copilot. |

| Vietnam promotes GenAI training programme for teachers A Generative AI skills training programme for teachers will be implemented on a national scale in Vietnam, promoting AI integration in education. |

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:

Related Contents

Latest News

More News

- FX pressures to persist but remain manageable in H2: HSBC (August 02, 2026 | 08:00)

- Citi Vietnam hosts AI Day to equip staff with digital skills (July 31, 2026 | 11:04)

- Fed holds rates steady for fifth straight meeting (July 30, 2026 | 17:30)

- Vietnam stocks rebound as analysts retain bullish outlook (July 30, 2026 | 16:39)

- Q2 earnings paint mixed picture across listed firms (July 30, 2026 | 16:37)

- MB chairman: Vietnam can be testing ground for globally scalable innovation (July 30, 2026 | 14:33)

- Manufacturing firms deliver stronger earnings on efficiency gains (July 30, 2026 | 12:40)

- Investment Support Fund Management Council reshuffled (July 30, 2026 | 12:18)

- Vietnam and World Bank align on 2026-2030 high-impact project lending pipeline (July 30, 2026 | 12:06)

- Global Forum helps Vietnam strengthen tax information exchange (July 30, 2026 | 12:04)

Mobile Version

Mobile Version